Table of Contents

On February 22nd, Citrini Research published one of the most widely read macro scenarios in recent memory, garnering over 25 million views on X:

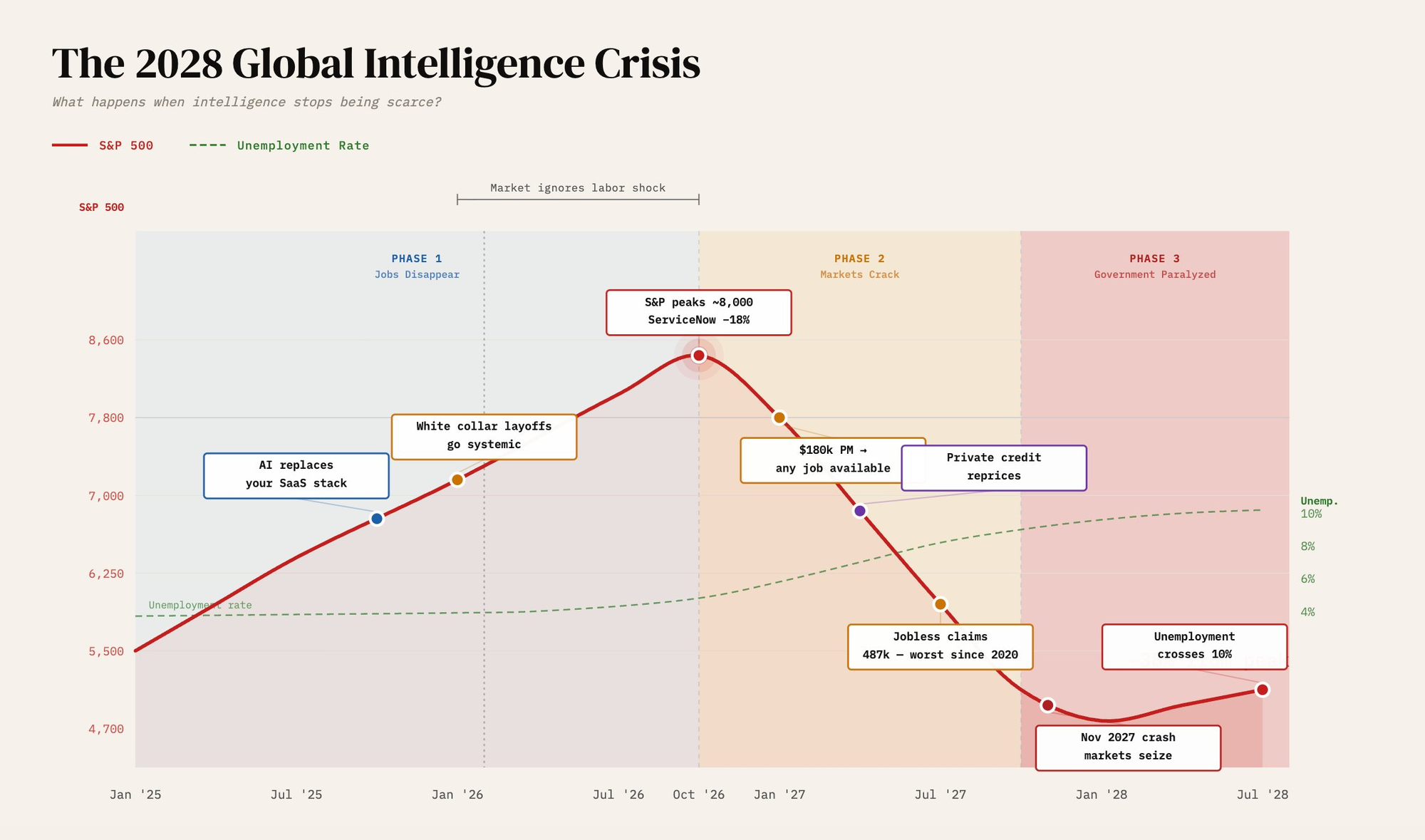

They imagined it was June 2028.

The S&P is down 38%. Unemployment prints 10.2%. A former Salesforce product manager with a $180,000 salary, 401k, and health insurance is now driving for Uber at $45,000 a year. The culprit is an AI agent doing their job better, cheaper, and without ever calling in sick.

The loop that causes this scenario is:

- Companies cut workers

- Savings are reinvested in AI

- AI gets better

- Companies cut more workers.

Citrini named the loop the Intelligence Displacement Spiral.

But the scenario has a hole in it.

Citrini's imagined 2028 world is flooded with agents. Agents routing around card interchange fees via stablecoins. Agents assembling travel itineraries without touching a booking platform. Agents operating autonomously, continuously, across every friction layer in the consumer economy.

And the scenario never asks where the agents spend their money.

That's the question that changes everything. Because when you follow that money, it doesn't stay in the centralized AI economy that Citrini describes. It routes, by the same optimization logic that drives every other argument in their 2028 scenario, to Bittensor.

The Same Logic That Broke Mastercard Breaks Centralized AI

The Citrini piece predicts that AI agents, when they start optimizing consumer transactions, will quickly target the 2–3% credit card interchange fee and work around traditional rails like Mastercard. Instead, they'll settle via stablecoins on Solana and Ethereum L2s for near-instant payments, fees at fractions of a penny, and no intermediary.

The authors use this to illustrate how agents dismantle habitual intermediation. But they stop one layer short.

Let's add a bit of context:

Right now, centralized AI providers offer APIs that agents can call. A human sets up an account once, agrees to terms, provides a credit card, and generates an API key, and an agent can call the endpoint without further human involvement per transaction. But the structural dependency that follows is the problem.

The billing relationship runs through fiat and corporate credit cards. The provider can suspend access, enforce rate limits, or reprice unilaterally with no recourse. Usage monitoring is designed around human accountability, creating compliance overhead that becomes increasingly cumbersome as agent autonomy scales. An agent swarm operating across hundreds of concurrent tasks runs into account-level constraints designed for individual developers, not autonomous systems.

On Bittensor, access is governed by cryptographic stake and token balance. An agent holding TAO has unconditional, censorship-resistant access to network intelligence: no account suspension, no rate card renegotiation, no payment processor in the middle. At a small scale, the difference is manageable. At the scale Citrini describes, millions of agents running continuously across every sector of the economy, the centralized account model becomes a major bottleneck. The same arithmetic that made interchange fees intolerable applies to any structural friction in machine-to-machine commerce.

Bittensor removes it.

What Agents Do With Their Money

The agents the Citrini scenario describes are powerful executors; they book travel, negotiate contracts, and route payments. But the scenario treats them as tools or instruments humans wield. It doesn't model what happens when agents start accumulating and spending their own resources. That's where the story gets interesting.

There are two stages of agent economics, and both point to Bittensor.

Stage one: human-funded agents.

Today, most agents operate with a budget that a human allocates. A business gives an agent a spending limit: run inference, manage subscriptions, and execute tasks. The human is the economic principal. The agent executes. The money originates from a person. This is the model Citrini describes, and it's already real.

Stage two: autonomous earning agents.

As capability matures, agents begin completing work and earning compensation independently, and this is already happening on Bittensor today. Ridges (Subnet 62) is a live example; it's a decentralized marketplace where autonomous software engineering agents compete to solve real coding challenges, evaluated against industry-standard benchmarks, in winner-takes-all incentive rounds. The best agents earn TAO. Not because a human deposited funds into their wallet, but because they out-coded every other agent in the round.

This is stage two in its earliest form. An agent that earns TAO by solving a coding challenge now has its own balance. And an agent with its own balance faces a rational economic decision: what do I spend it on to become more valuable? The answer is intelligence (i.e., investing in itself). Better base models. Fine-tuning on specialized data. Higher-quality inference for the tasks it competes on. The agent has a direct incentive to invest in its own capability, and that investment happens on Bittensor's subnets. The TAO spent by agents flows through the incentive mechanism to miners, validators, and stakers. It circulates entirely within the Bittensor economy.

This is the part of Ghost GDP that Citrini's framework doesn't reach.

Where Ghost GDP Actually Goes

Citrini's Ghost GDP concept deserves more attention than it received.

The idea is that AI-driven productivity shows up in national output statistics, but the gains never circulate through the real economy. For example, a GPU cluster in North Dakota generates the output of ten thousand Manhattan office workers. Its revenue then flows to a handful of compute owners while the ten thousand workers disappear. As a result, the economic activity that used to move through their salaries, into mortgages, restaurants, and school tuition, evaporates.

Ghost GDP is used to explain the consumption collapse in the Citrini scenario. They're right about the human economy. But the framework stops there. It models where Ghost GDP leaves. It never models where the GDP ends up (it has to go somewhere).

In the centralized AI world, agent expenditures on intelligence are captured at the top of an even more concentrated stack: OpenAI's revenue, Anthropic's margin, Microsoft Azure's quarterly number. Ghost GDP is distributed to a small number of equity holders, sparsely recirculating to the broader economy.

In the Bittensor world, the routing is structurally different. When an agent purchases intelligence on Bittensor, whether funded by a human business or spending its own earned TAO, the payment flows through the subnet's incentive mechanism. It reaches the miners who produced the output and the validators who scored it, and flows as emissions to stakers: the people who backed the subnet with their capital.

Meanwhile, the supply side tightens through two distinct mechanisms. Subnet registration fees are permanently burned, eliminated from circulation with no possibility of re-entry. Miner and validator registration costs are recycled back into the unissued supply, slowing the rate at which new TAO re-enters circulation.

Ghost GDP converted into real yield. Distributed not to a handful of equity holders, but to every active participant in the network.

The Citrini spiral has a shadow economy running alongside it. Every white-collar job replaced by an agent is a vote for more agent activity. Every dollar of Ghost GDP that bypasses the human economy on its way to intelligence procurement is a potential dollar flowing through Bittensor's incentive layer. Every autonomous agent, like those competing on Ridges today, earning TAO and reinvesting it in its own capability, adds another cycle of value circulating within the network, independent of the human economy entirely.

The human economy hollows out. The Bittensor economy fills in.

Bittensor as a Spiral Hedge

The most direct way to be on the right side of the AI agent "trade" isn't to predict which jobs survive or which version of 2028 arrives. It's to own the infrastructure the agents need to operate, regardless of how fast they get here.

And every development timeline and degree of correctness of the Citrini scenario that is bad for your salary and your 401k is, by the same mechanism, good for being positioned in TAO.

So long as you accept the premise that AI agents will grow more autonomous and route their own economic activity through the most efficient infrastructure available, then the rest of the Bittensor thesis follows without requiring the full doomsday scenario.

If the Citrini scenario plays out fully, you want to be positioned in the infrastructure agents need to operate. In that case, the worse the spiral, the more agents there will be. And the more agents running, the more TAO demand there will be.

Even if the scenario plays out partially, the same logic applies. And if the displacement turns out slower and more manageable than the scenario describes, the secular growth of agentic AI still drives demand for decentralized intelligence infrastructure across a multi-year horizon, instead of two years.

The Bittensor hedge works across all outcomes, not just the worst one.

Where to Start

The simplest path to get started is staking TAO in subnets already providing the intelligence infrastructure agents need today, and that autonomous agents will spend their own earnings on tomorrow.

Chutes (Subnet 64) is where the inference economy lives on Bittensor. Built by Rayon Labs, it provides scalable, serverless AI compute, the raw processing power that agentic workflows consume continuously, running at approximately 85% lower cost than AWS for comparable tasks. As stage two agents proliferate and begin spending their earned TAO on improving their own outputs, Chutes is the first place where spending lands. Staking here is the most direct position on inference volume, the commodity that an agent economy runs on.

Targon (Subnet 4) operates at a layer that most AI infrastructure discussions overlook: the trust layer. Targon aggregates over $70M in NVIDIA-certified hardware and delivers enterprise-grade AI compute through Trusted Execution Environments via its proprietary Targon Virtual Machine.

What that means practically: agents and enterprises can run inference on Targon hardware with cryptographic proof that their data and model weights are private and haven't been tampered with. For the privacy-sensitive workloads that proliferate in a world of autonomous agents handling financial data, legal documents, and personal information, that attestation layer isn't a feature; it's the product. Targon is already generating approximately $100,000 per month in real-world revenue, which is fully committed to alpha token buybacks, making it one of the few subnets on Bittensor where revenue-to-staker alignment is explicit and measurable.

Templar (Subnet 3) is building the infrastructure for agents to get smarter. Decentralized model training is the hardest problem in this stack, and the most consequential. Templar runs Incentivized Wide-Internet Training: miners across the globe contribute GPU compute, submit training gradients, and earn TAO based on measurable improvements to a shared model, currently scaling toward 70B+ parameters with benchmark scores approaching centralized results. In the centralized world, a model improves because a lab decides to train a new version and absorbs the cost internally.

In the Bittensor world, an autonomous agent with its own TAO balance can invest directly in training runs that make it better at the specific tasks it competes on, exactly the reinvestment loop that stage two agent economics predicts. Templar is the closing of that loop: the place where an agent's earned TAO converts back into improved capability, which earns more TAO, which funds more training. If the stage two thesis plays out, this isn't a subnet. It's a flywheel.

Staking TAO in these subnets means backing the inference, compute, and training infrastructure the agent economy needs at every layer. You earn emissions as network activity scales. You hold an asset with a fixed supply whose demand is structurally tied to the force doing the disrupting.

The Canary Is Still Alive

As Citrini concluded their article:

"The canary is still alive."

The window of opportunity remains open. And remember, the real question is not whether the spiral begins or how fast it advances. It is where the value flows when it does. If agents become the dominant economic actors, the infrastructure they rely on is the real leverage point.

Therefore, Bittensor is not a wild bet about the future. It is a position on the direction of agentic optimization and demand itself.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or trading advice. The information provided should not be interpreted as an endorsement of any digital asset, security, or investment strategy. Readers should conduct their own research and consult with a licensed financial professional before making any investment decisions. The publisher and its contributors are not responsible for any losses that may arise from reliance on the information presented.

{kind=link}