Table of Contents

The total market cap of all subnet Alpha tokens reached approximately $1.12 billion by March 2026, equivalent to around 27% of TAO's own market cap, across 128 active subnets. A meaningful share of that capital belongs to subnet owners and miners whose tokens are pending the BIT-0011 implementation currently in community discussion.

When a subnet owner needs cash, the only way to get it is to sell their Alpha tokens. But each subnet runs its own liquidity pool, and that pool sets the token's price. When the owner sells into their own pool, they push the price down, alarm their stakers, and undermine the very signal of confidence the market uses to allocate emissions to their subnet.

Alpha as Collateral is the Next Big Unlock for Bittensor

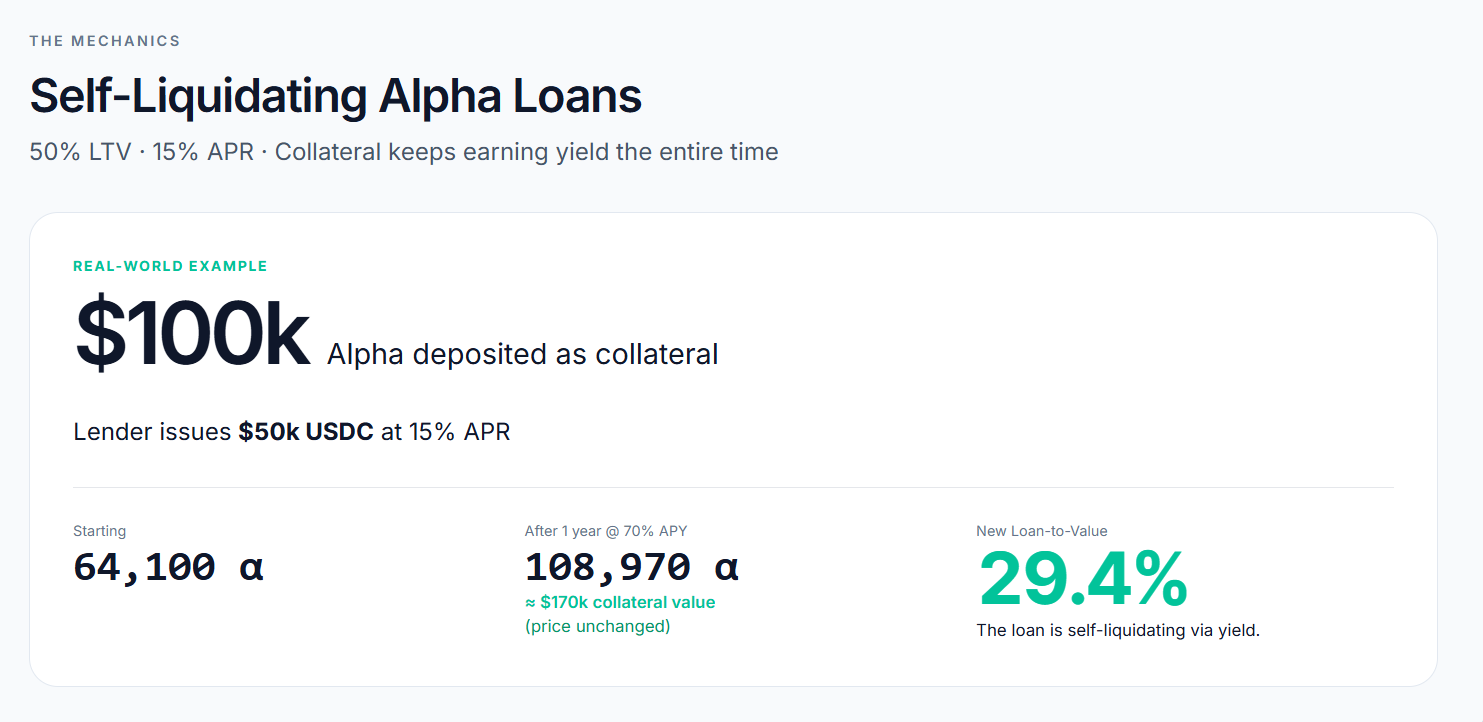

The Alpha Collateral deck, created by Siam Kidd, defines the structure: 50% loan-to-value, 15% APR, USDC disbursed against Alpha collateral, with automatic liquidation triggered above 70% LTV.

To understand why this works, we'll start with what makes Alpha tokens different from most collateral. Alpha tokens earn yield continuously. Every block, the Bittensor protocol distributes TAO emissions to subnet stakers, compounding their position automatically. A borrower who deposits Alpha as collateral is an asset that keeps growing while it sits in the lender's custody.

The numbers from the deck make this concrete. A borrower deposits $100,000 worth of Alpha, starting at 64,100 tokens. After one year at 70% APY, that position grows to 108,970 tokens, worth approximately $170,000 at an unchanged token price. The loan-to-value ratio drops from 50% to 29.4% without the borrower repaying a dollar. The yield on the collateral is retiring the loan on its own.

For a lender, this is structurally different from any traditional secured loan. In traditional lending, collateral is passive. A house does not pay down a mortgage by itself. A stock portfolio requires active management to generate yield. Here, the collateral is actively compounding, which means the lender's risk exposure shrinks over time without any action from the borrower. Add automatic on-chain liquidation above 70% LTV, and the lender has a defined ceiling on downside that executes in minutes rather than months. On $20 million in lending TVL, that structure generates $3 million per year, or $250,000 per month, with minimal discretionary risk management required.

What Locked Stake Is and Why It Makes This Urgent

To understand why a lending product matters so much right now, you need to understand what Bittensor is about to do to liquidity.

BIT-0011, the Locked Stake proposal introduced by Bittensor co-founder Jacob Steeves on April 16, 2026, came directly out of the Covenant AI crisis. That event saw founder Sam Dare sell 37,000 TAO worth approximately $10 million, triggering a 25% drop in TAO price and exposing a fundamental governance gap: nothing stopped a subnet owner from building a large position, earning community trust, and exiting without warning.

BIT-0011 fixes this with a simple but powerful mechanic. Subnet owners lock their Alpha tokens for a chosen period, anywhere from months to years. That lock produces a conviction score calculated as stake multiplied by time remaining. The score starts at 100% of the locked value and decays linearly as the lock period approaches expiry. Every 30 days, the network recalculates scores using an Exponential Moving Average to prevent short-term manipulation. The participant with the highest conviction score on a given subnet has the opportunity to own it. If that score decays below a challenger's score, ownership can transfer.

Critically, locked tokens cannot be moved or unstaked until the lock expires. There is no early exit. This is the core protection the protocol was missing before Covenant departed.

The result for Alpha holders is genuine transparency. Every subnet owner's conviction score is publicly visible on-chain. Stakers can see exactly how much Alpha an owner has locked and for how long before committing their own capital.

Therefore, BIT-0011 creates a credit opportunity that did not exist before. An owner who locks 200,000 Alpha for 12 months to prove conviction now holds an asset that earns yield, signals long-term commitment on-chain, and produces zero spendable dollars for a full year. The lock is the credential. It tells the market the owner is serious. It tells a lender that the owner cannot run. A lending product that accepts locked Alpha as collateral converts that frozen credential into working capital without touching the lock itself. The owner keeps their conviction score, keeps their upside, and walks out with USDC.

The owners who lock the most Alpha are precisely the ones a lender wants as borrowers: operators publicly committed on-chain, earning yield continuously, and unable to exit without forfeiting the subnet they spent months building.

The Loop That Bids Up Everything

The Alpha Collateral deck identifies a demand dynamic that extends well beyond the direct loan transaction. A borrower receives USDC, uses it to buy TAO on the open market, stakes that TAO into more Alpha, and increases their collateral position while bidding up prices. That lowers their own LTV further and allows early loan repayment with fewer tokens than originally pledged.

Each cycle of that loop injects new buy pressure into TAO and the relevant subnet's Alpha simultaneously. The lender's collateral appreciates, the borrower's LTV improves, and the subnet's on-chain liquidity deepens with every rotation, all with zero tokens sold.

BIT-0011 reduces liquid supply by locking capital in place for governance. A lending layer reduces sell pressure from a separate direction by giving owners an alternative to liquidating. The two mechanisms reinforce each other rather than compete.

Nine Figures in Collateral Is Waiting for One Institution

The addressable collateral base for a first-mover lender is already nine figures before accounting for anything below the top ten subnets. The top 10 subnets alone carry a combined valuation of approximately $712 million as of March 2026, and 118 more subnets sit beneath them on the same infrastructure. On-chain AMM pricing gives any lender a real-time collateral valuation feed. Automatic liquidation at 70% LTV gives them a defined risk ceiling with no discretionary judgment calls required.

In 2025, Bittensor introduced EVM compatibility, lowering the barrier for developers to deploy smart contracts and build DeFi applications directly on the network, with borrowing and lending protocols among the named use cases. The smart contract rails are already built. TAO's network staking reward rate currently sits at approximately 17.33%, meaning the collateral underlying any Alpha loan yields more on an annualized basis than the 15% APR charged to the borrower. The yield on the asset covers the cost of the loan before the borrower touches a dollar of principal.

The lender that enters this market first gets a borrower base with no alternatives, yield-bearing collateral that outpaces its own interest rate, and real-time liquidation infrastructure that traditional secured lending has never had.

You're either the institution that built the product when the collateral was $1 billion, and the competition was zero, or you're reading this after someone else already did.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or trading advice. The information provided should not be interpreted as an endorsement of any digital asset, security, or investment strategy. Readers should conduct their own research and consult with a licensed financial professional before making any investment decisions. The publisher and its contributors are not responsible for any losses that may arise from reliance on the information presented.

{kind=link}